Anyone who’s keeping up with digital in government or changes to the conveyancing sector will have spotted references to our research and development project, Digital Street.

The project has now started its second year, and in a few weeks, we’ll have a video looking at the work done so far in year 1. In the meantime, we wanted to give you a preview look at the prototype services we came up with.

The point of Digital Street is to give HM Land Registry a space to break away from the constraints and current ways of thinking about the home buying process as it stands today. We wanted to explore how we could use technology to revolutionise land registration and conveyancing.

We started with users. We organised a series of workshops and research sessions with people who are involved in land registration and conveyancing. We talked to conveyancers, estate agents, mortgage lenders, homebuyers, and sellers. Among other things, we asked them:

How do you see technology changing your role, or your organisation, over the next 10 years?

Three proofs of concept

We used the research insights to develop a set of digital mock-ups that show what could be possible. A hackathon helped us develop these ideas further, and turn them into proofs of concept that we can show to other people.

In the spirit of “showing the thing”, here’s a quick look at each of them. Keep in mind that these are all early prototypes, with rough edges and missing parts. They’re a way of showing our ideas for what’s possible.

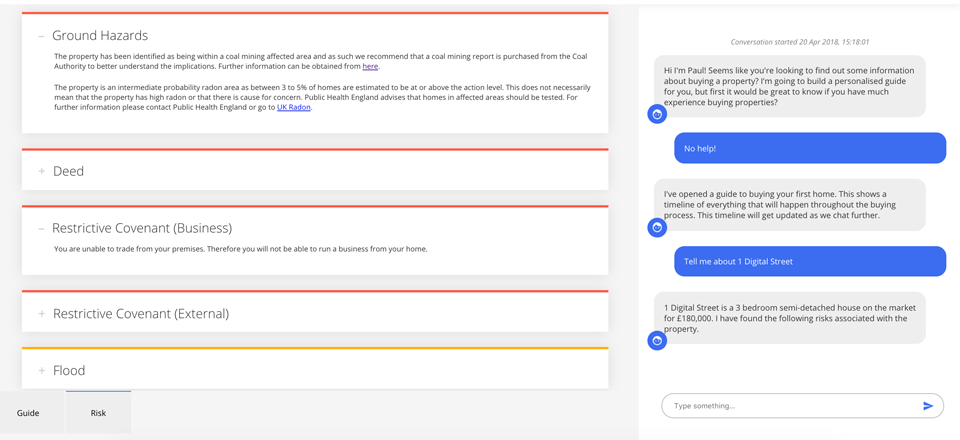

Concept 1: Property assistant

In this mock-up, homebuyers can ask questions in plain English, and get instant help and advice about the steps they need to take to buy a home. Our thinking here was that making things easier to understand up front means users can make more informed decisions, earlier in the process.

For example, it’s common for people to get emotionally attached to a property they’d like to buy, and to start spending money on doing that, only to find out many weeks later that there’s a problem they didn’t know at the start. Maybe the property is at high risk of flooding, or they can't park a van on their drive, or run a business from the property. Showing this sort of information to users earlier might avoid these unexpected surprises.

The chat interface would be just like sending an SMS message to a human being, but behind the scenes, the answers would be provided by software making use of state-of-the-art machine learning techniques to interpret the known data about a property.

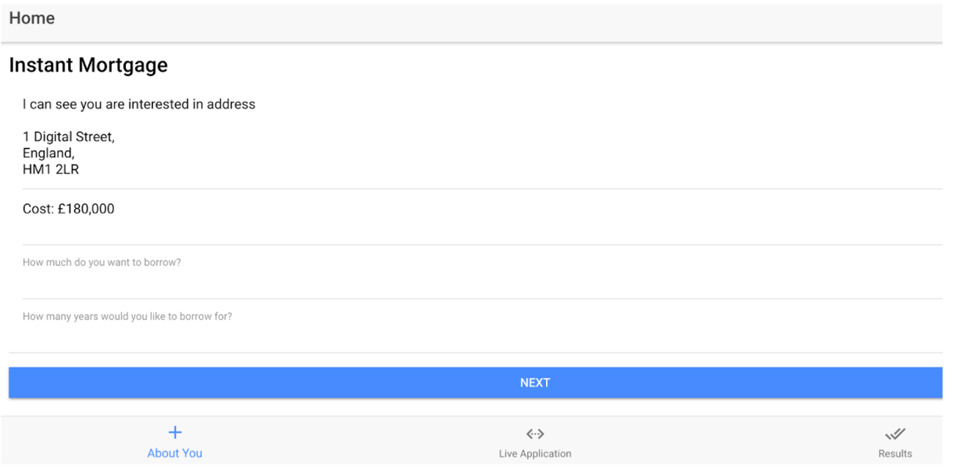

Concept 2: Instant mortgage

Here, we tried to imagine new ways of approving mortgages for homebuyers.

An app would look for relevant information about the homebuyer and the property they were interested in buying. It could check the register and other property data sources for any known potential risks, and if there were no complications, offer up a list of pre-approved mortgage deals from a variety of lenders.

Again, this is about speeding up the home buying process by connecting up the right information from the right sources earlier.

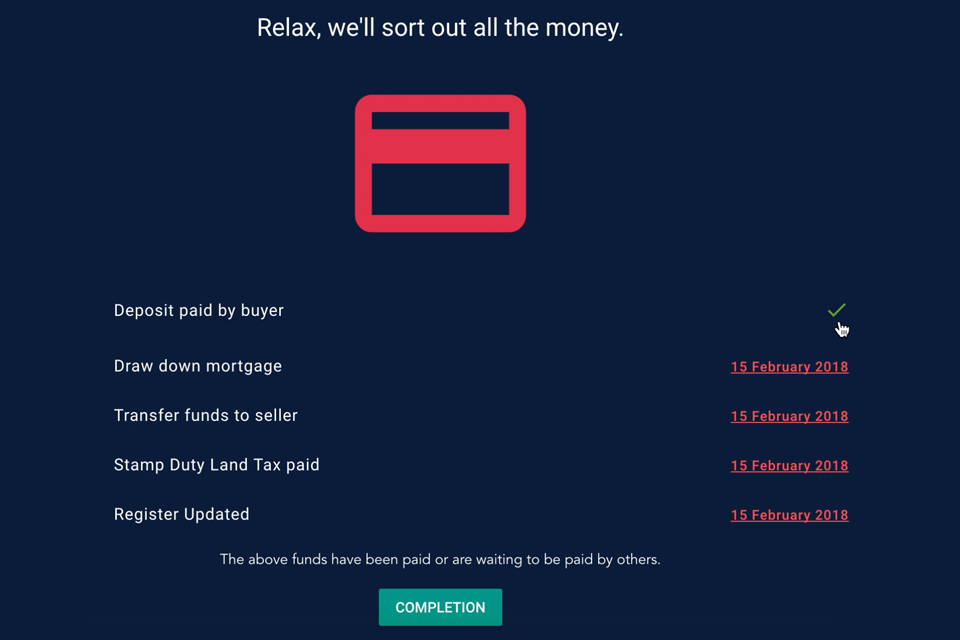

Concept 3: Property exchange assistant

Finally, we looked at the sometimes stressful process of exchanging and completing on a house purchase.

This concept shows an online service which digitises both processes using smart contracts, as well as automating the transfer of funds and updating the register using blockchain or digital ledger technology.

This is our way of thinking out loud

We’re not saying that we, or the industry, should ever develop these specific proofs of concept in real life. What we are saying is that services like this, using technologies like these, are the kind of thing we should all be considering. We should be ambitious. We should be bold. Technological change will only continue to accelerate. It’s important that we become an organisation that can respond to that change, and make best use of it. Research like this helps us do that.

If you’d like to see more of these proofs of concept, you’ll see it in the video demo that we plan to publish soon.

8 comments

Comment by Ann Foster posted on

Looking forward to hearing more about your new scheme and seeing the video.

Comment by John Harvey posted on

To paraphrase Sartre, the complicating factor of any home move is the involvement of many people and entities over which you have no control.

Your buyer's ', buyer's ', buyer's ', buyer's ', mortgage broker's inefficiency can stop you getting your kids into a new school at the start of term.

Such a process is not fit for purpose.

Moving home (almost inevitably) involves a chain and needs supply chain management expertise to organise it. But this is rarely present -if at all..

Hope the video will cover this.

Comment by ianflowers posted on

John - thank you for your comment. We do agree that this is one of the key 'pain points' with the home buying process today and came out in our research last year. The third proof of concept (property transaction) explored how we could increase the transparency of the process so that users could see where they are in the process. It also looked at how we could use automation instead of having to rely on manual processes to make things happen. We will continue to explore how we can solve this problem by working alongside the industry in our second year of research and development.

Comment by Tom White posted on

Good to read Lauren, all great sounding stuff!

Comment by Mike Bowen posted on

If we have data available at point of sale a move to a reservation agreement system becomes more viable. This needs all data to be available buyers to have mortgages agreed in principle (open banking will help) and a huge change in mindset among lawyers lenders and agents and also the consumer. The provision of data is key and LR are helping with this already.

Comment by C Goodwin posted on

In the same way that the banks have found it necessary to protect digital data transactions by the use of a customer pin number, do you think it would be a good idea for registered proprietors to have their own individual pin number (since dematerialisation has taken away the protection previously provided by the possession of the title deeds)?

As the asset is likely to be the most expensive one owned, would it also be a good idea for them to have a number verification device ?

Comment by Lauren Tombs posted on

Thank you for your comment and your idea. The team will be exploring a number of ways of how we might digitally transact on a property in future and particularly how you link an owner to a property. We will ensure that we post regular updates on the project’s progress.

Comment by Leighton posted on

Hi, There is a bitcoin fork being prepared now specifically for the transfer of assets on a proof of work decentralised open source Blockchain.

The project is called Ravencoin and it is a very interesting project when you are looking at transfering and keeping assets on a secure blockchain.

https://getravencoin.org